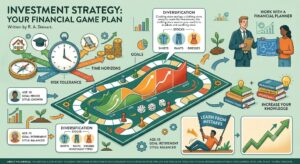

Investment Strategy

Written by R. A. Stewart

Because investing is not a sure thing in most cases, it is much like a game – you don’t know the outcome until the game has been played and a winner has been declared. Anytime you play almost any type of game, you have a strategy. Investing isn’t any different – you need an investment strategy which is based on factors such as your age, your goals, and your personal circumstances.

An investment strategy is basically a plan for investing your money in various types of investments that will help you meet your financial goals in a specific amount of time. Each type of investment contains individual investments that you must choose from. A clothing store sells clothes – but those clothes consist of shirts, pants, dresses, skirts, undergarments, etc. The stock market is a type of investment, but it contains different types of stocks, which all contain different companies that you can invest in.

Your financial plan must be one which fits in with your personal circumstances and not something which you feel you should do just because others are doing it. Making choices which will enable you to live within your means is at the heart of money management, it is not the size of your pay packet which counts it is what you do with it which determines how much you have by the following pay day.

If you haven’t done your research, it can quickly become very confusing – simply because there are so many different types of investments and individual investments to choose from. This is where your strategy, combined with your risk tolerance and investment style all come into play. There are plenty of books available on finance and investing. Reading these books will increase your financial literacy with the result that you make better choices in the future.

If you are new to investments, work closely with a financial planner before making any investments. They will help you develop an investment strategy that will not only fall within the bounds of your risk tolerance and your investment style, but will also help you achieve your financial goals.

Never invest money without having a goal and a strategy for reaching that goal! This is essential. Nobody hands their money over to anyone without knowing what that money is being used for and when they will get it back! If you don’t have a goal, a plan, or a strategy, that is essentially what you are doing! Always start with a goal and a strategy for reaching that goal!

Your goals are the factors which determine where you should invest your money. If the money is for your retirement then growth funds may be the answer to where to invest but this all depends on how long to go before you retire and when you are likely to need that money.

Never beat yourself up for making the odd mistake and never let it deter you from making future investments. Learn from your mistakes and learn from them. In this way you will become a better investor.

ABOUT THIS ARTICLE

This article is for information purposes only and is not financial advice, it is of the opinion of the writer and may not be applicable to your personal circumstances, therefore discretion is advised.

Read my other articles on www.robertastewart.com

Working in your chosen field

You may not have the talent or inclination to be an international sportsperson but you can be an asset in your chosen field and that does not mean that you have to be something out of the ordinary to become a valued member of society. A person who works at an entry level job can do so with such a good attitude that their diligence will not go unnoticed by their employers.

You may not particularly like your job and have any control over what happens at work but your attitude is something you can control. An employer with a bad attitude will take that bad attitude with them wherever they go.

If you enjoyed this article then this ebook may interest you: